In Q1 2026, institutional investors poured $18.7 billion into spot BTC ETFs. BlackRock's IBIT absorbed $8.4 billion of that in three months, bringing its AUM to $54 billion. Public companies hold more than 1.16 million BTC on their balance sheets, which accounts for over 5.5% of all BTC that will ever exist.

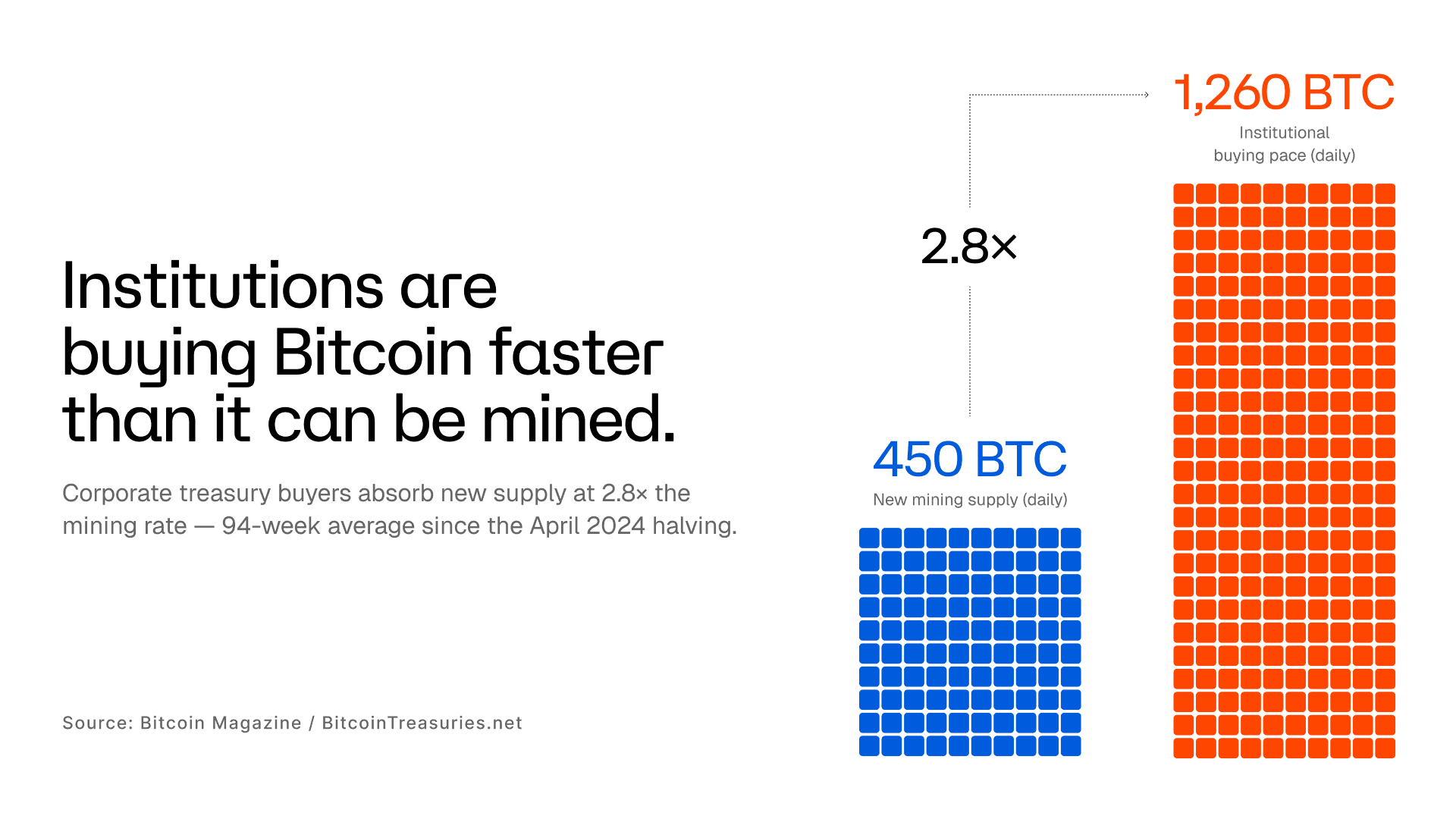

Today, institutions are buying at 2.8 times the rate new Bitcoin is being mined. So, the allocation decision is made, but the issue of yield remains unresolved.

Bitcoin ETFs generate no yield. Direct custody generates no yield. Corporate treasury Bitcoin generates no yield. Hundreds of billions sit in an asset that produces nothing while it holds, no coupon, no dividend, no interest payment. Meanwhile, custody and holding fees clock on regardless. In any other asset class, that would be a design flaw. After all, a bond that paid no coupon would not be a bond. Real estate that generated no rent would be akin to a vacant lot.

The Second Wave Hitting BTC Wants Yield

In March, Coinbase published research on what they called the second wave of institutional money entering crypto. While the first wave came for price appreciation, this second wave is hunting yield. The kind of income that can be modeled, reported, and explained to a risk committee. Institutions have now shifted from asking whether to hold BTC and started asking what holding it should produce.

Also in March, the SEC and CFTC issued joint guidance clarifying how federal securities law applies to crypto assets. The legal uncertainty that kept institutional compliance teams sidelined for years has substantially lifted. Around 73% of institutional investors now plan to increase digital asset allocations in 2026, but what remains to be built is the infrastructure to support it.

The yield products that exist weren't built for institutional capital. Lending platforms that promised yield in 2022 collapsed because their structures were overleveraged and opaque. DeFi protocols generate real returns, but they expose capital to smart contract risk, governance votes made by anonymous token holders, and counterparty relationships that cannot be legally enforced. These documented failures are the specific reasons institutional compliance departments reject Bitcoin yield proposals.

hemiBTC is the Answer

What institutional BTC holders are asking for is yield on what they already hold, through a structure that maintains custody, and fits inside existing compliance frameworks.

hemiBTC does this. Institutions activate yield on native BTC on Hemi with various DeFi protocols, without transferring custody, without wrapped tokens that introduce centralization risk, and without the added risk of leveraged or rehypothecated structures. The yield is generated through onchain activity on Hemi's infrastructure, not from lending into opaque networks, or from selling covered calls on price exposure.

The 2022 collapses were predictable, but not exceptional. They were the result of yield built on rolling leverage rather than genuine economic activity. Institutional capital knows this, and it likely won't return to that model regardless of the return on offer. What institutions are more prepared to engage with are yield mechanisms that can be explained to a compliance team, a risk desk, and a client without any of those conversations ending badly.

The $18.7 billion in Q1 is a starting point. The institutions that got into BTC for price exposure are now asking what else it should do. Hemi is where that happens.

See more about what BTC can do for you on the Hemi Portal.